Month in Review as at March 2023

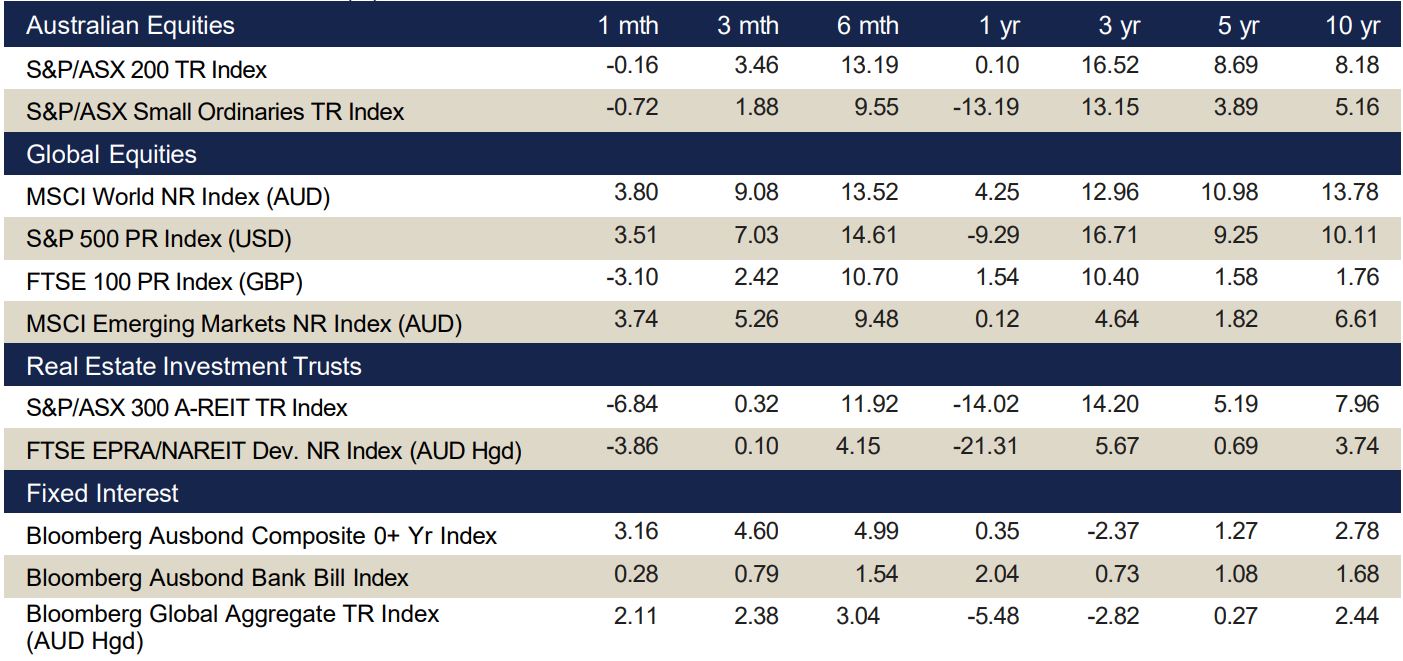

VIEW PDFIndex returns at end March 2023 (%)

Data source: Bloomberg & Financial Express. Returns greater than one year are annualised.

Commentary regarding equity indices below references performance without including the effects of currency (unless specifically stated)

Key Points

- Australian equity market was down in March with S&P/ASX 200 Index returning -0.2% driven by banking contagion fears.

- Globally, developed markets recovered following the expectation of monetary easing with the S&P 500 Index (USD) gaining 7% and the FTSE Eurotop 100 Index (EUR) returning 1.0%.

- In Asia the Hang Seng Index (HKD) generated a return of 3.5%, while the CSI 300 Index (CNY) finished -0.5%.

Australian equities

The month of March ended with the S&P/ASX 200 Accumulation Index down -0.2%. The primary driver was the uncertainty arising from bank failures in the US and Europe. This, coupled with high, albeit easing, inflation added to investors’ uncertain market sentiment. The Materials sector (+5.9%) rebounded with Communications (+3.4%) also performing strongly while the Property (-6.8%) and Financials ex-Property (- 4.9%) sectors were the worst performers. Over the quarter, Consumer Discretionary (+11.4%) was the best performing sector.

Materials led all sectors for the month, reaping the benefits of higher commodity prices. The Property sector sold off following concerns around commercial real estate valuations, which stemmed from investor sentiment around higher interest rates and macroeconomic headwinds. Meanwhile, the collapse of major overseas banks led to selloffs within the Financials ex-Property sector. Overall, investors grappled with the inflation-driven interest rate outlook facing central banks globally and its implications on future economic outlook.

Global equities

Global equities rallied after a sharp initial decline for the month, led by volatility across the Financial Services sector, notably Silicon Valley Bank and Credit Suisse. This was alleviated with expectations of potential easing in central bank tightening via the US Fed’s dovish outlook commentary for the year. Emerging markets performed similarly to developed market counterparts returning 3.7% (MSCI Emerging Markets Index) and 3.9% (represented by the MSCI World Ex Australia Index) in Australian dollar terms, respectively.

Investor confidence was maintained as relatively positive, with global macro data continuing to the upside. Mixed performance was seen across Asia, with China posting fresh economic stimulus geared towards growth, as well as varied reception to the Fed’s dovish comments. This was reflected by the Hang Seng Index and the CSI 300 Index, returning 3.5% and -0.5%, respectively (in local currency terms) for the month. In the US, indications of no further rate rise lead the rebound, with the S&P500 Index posting a monthly return of 3.7%

Over in Germany, the DAX 30 Index reported a gain of 1.7% for the month (in local currency terms) after posting decreasing manufacturing data indicating further weakness ahead, which was shared by the rest of the continent with the FTSE Eurotop 100 Index reporting similar returns of 1.0% (in local currency terms) for the month.

Property

The S&P/ASX 200 A-REIT Accumulation index continued to fall in March after selling off in February, with the index finishing the month –6.8% lower. Global real estate equities (represented by the FTSE EPRA/NAREIT Developed Ex Australia Index (AUD Hedged)) also regressed, returning -3.6% for the month. Australian infrastructure continued its positive momentum during March, with the S&P/ASX Infrastructure Index TR advancing 0.3% for the month.

March was relatively quiet across the A-REITs sector. Some activity includes Centuria Capital Group (ASX: CNI) announcing the acquisition of a NSW glasshouse. The deal is worth $323m and is an addition to their agriculture fund which has seen rapid growth since inception. This acquisition increases the group’s total agriculture AUM to over $500m and cements Centuria as Australia’s biggest large-scale glasshouse landlord.

The Australian residential property market increased by 0.8% month on month in March represented by Core Logic’s five capital city aggregate. Sydney (+1.4%) and Melbourne (+0.6%) were the best performers whilst Adelaide (-0.1%) was the only city to regress during March.

Fixed Income

At the start of March, the RBA raised the cash rate target by 25bps to 3.6%, stating global inflation remains high and is expected to take some time before it returns to target rates, while growth in the Australian economy has slowed and is expected to be below trend. However, uncertainty within the global financial sector was reflected across the Australian 2- and 10-year Government bond yields which fell by 70bps and 56bps, respectively. Australian fixed income performed strongly during the month with the Bloomberg Ausbond Composite 0+ Yr Index returning 3.2%.

Globally, markets were jolted by the financial sector woes in the US and Europe, which significantly impacted financial conditions and bond yields during the month. A California-based regional bank (SVB) failed, leading to the second biggest US bank failure in history, and a further two regional banks went into administration.

Over in Europe, UBS’s takeover of Credit Suisse caused turmoil in bond markets, with Swiss authorities allowing Credit Suisse’s riskiest bonds to be wiped out, and equity holders receiving a small amount of equity in UBS as part of the transaction. The US 2- and 10- year Government bond yields fell by 80bps and 45bps, respectively. The Fed continued to raise rates for the ninth consecutive time to 4.75%-5%, demonstrating their commitment to ending the inflation problem despite the banking crisis. In the United Kingdom, GILT yields followed the US, as 2- and 10-Year Gilt yields fell 60bps and 22bps, respectively.

Key points

- Central banks moved swiftly to avoid banking collapse with Credit Suisse bought out by UBS and emergency cash provided to several US banks.

- RBA increased the cash rate by 25%, taking it to 3.6%.

- Both the Fed and ECB raised interest rates in response to persistently high inflation.

Australia

The RBA increased the cash rate by 25bps at its March meeting, bringing the rate to 3.6%. The annual inflation rate slowed to 6.8% in February, led by smaller rises for fuel and housing, adding to evidence that the worst of the price increases has passed.

February’s unemployment rate was 3.5%, against expectations of 3.6%, with the economy adding 64,600 jobs. Retail sales rose 0.2% in February, suggesting that retail turnover has levelled out after the volatility of the previous three months.

The Westpac-Melbourne Institute Index of Consumer Sentiment for March was unchanged at 78.5 with areas of most concern being inflation, interest rates and the general economy. Composite PMI fell to 48.5 in March as manufacturing and service sectors recorded declines in activities that led to a broad deterioration in private sector output. The NAB business confidence index came in at 16 in March, well above its long-run average.

The trade surplus increased to $13.9 billion in February, above the market forecasts of $11.1billion.

Global

March was tumultuous month for markets as several small/mid-sized banks in the US shut down and depositors redeemed their money as questions about the viability of these banks gained momentum. This was followed by one of the cornerstone establishments of Swiss banking, Credit Suisse, being bought out by UBS to avoid a banking collapse and possible contagion across the global banking sector.

While these bank failures may have bought back memories of the GFC of 2008, the sector as a whole has significantly de-risked since 2008, notably in terms of increased Tier 1 capital ratios. Central banks also quickly stepped in with the provision of emergency cash, which seemed to settle markets.

US

The Federal Reserve raised the cash rate by 25bps to 5.00% in March as inflation remained elevated. Inflation came in 0.1% higher for March, against expectations of 0.3%, bringing the annual rate to 5.0%.

Non-farm payrolls added 36,000 new jobs in March. The unemployment rate edged down to 3.5% in March, better than market expectations of 3.6%.

Consumer confidence increased in February to 104.2 but remains below the average seen last year. Retail sales fell 0.4% month-on-month in February, more than the expected 0.3% fall.

The S&P Global Composite PMI rose to 52.3 in March, showing a modest rise in business activity mainly led by a steeper increase in service sector output. PPI dropped 0.1%in February against market expectations of a 0.3% increase, with the annual rate easing to 4.6% and missing the market forecast of 5.4%.

Balance of trade deficit widened to US$70.5 billion in February, above the expected US$69 billion.

Euro zone

The ECB increased the cash rate by 50bps to 3.5% in its March meeting as inflation is projected to remain too high for too long. The ECB released revised inflation forecasts and now see inflation averaging 5.3% in 2023, 2.9% in 2024 and 2.1% in 2025, with underlying price pressures remaining strong.

The annual inflation rate came in at 6.9% in March below the expected 7.1%, signaling that inflationary pressure remains high in Europe. Unemployment remained steady at 6.6% in February against expectations of 6.7%.

Consumer confidence edged down to -19.2 in March as consumers were less positive about the economy. Retail sales dropped 0.8% in February, matching market expectations, with the annual rate coming in at -3.0%. January’s unemployment rate came in at a record low of 6.6%, slightly below market expectations of 6.7%.

The Composite PMI rose to 53.7 in March, helped by the strongest increase in service sector activity in 10 months. PPI dropped 0.5% % in February, more than the expected -0.3% decrease, with the annual rate easing to 13.2% below the anticipated 13.3%.

UK

The Bank of England raised rates by 25bps to 4.25% in March, on the back of persistently high inflations. GDP posted a 0.1% increase in 4Q22, expanding on the 0.1% decline in the prior month whilst the annual rate came in at 0.6%.

Inflation unexpectedly rose 1.1% in February, bringing the annual rate to 10.4%, well above the expected 9.9%. This jump was largely due to surging food price inflation which is running at 18%.

Consumer confidence rose to -36 in March, matching market expectations. The annual retail sales rate rose 5.1%, well ahead of the 12-month average of 2.6%. in March, buoyed by Mother’s Day spending.

The composite PMI index fell dropped to 52.2 in March, supported by increased output in both the manufacturing and service sectors.

PPI fell 0.3% in February, missing the market expectations of a 0.2% rise, with the annual rate easing to 12.1%, slightly below the anticipated 12.4%.

China

The Chinese government set a growth target of 5% for 2023, which it acknowledges will not be easy to achieve. The country’s economic rebound remained uneven in March with the services sector seeing a strong recovery but the manufacturing sector losing momentum amid still-weak export orders. The annual inflation rate unexpectedly came in at 0.7% in March 2023, compared with market consensus of 1.0%.

The unemployment rate increased to 5.6% in February. Retail sales expanded 3.5% from the prior year in combined figures for January-February 2023, matching market consensus and shifting from a 1.8% fall in December.

Composite PMI increased to 54.5 in March, the third straight period of growth in private sector activity and the strongest pace since last June amid the removal of strict pandemic measures.

Asia region

The Bank of Japan maintained its key short terms interest rate at -0.1% at its March meeting.

Inflation decreased 0.6% month on month and to 3.3% annually in February, the lowest rate since last September as fuel and electricity charges dropped for the first time since May 2021.

The unemployment rate unexpectedly rose to 2.6% in February, above the 2.4% forecast.

The consumer confidence index rose to 33.9 in March, above market forecast of 31.9, as households’ sentiment strengthened across all indices. Retail Sales in Japan decreased 4.4% in February, with the annual rate rising 6.6%, exceeding the market expectation of 5.8%.

The Composite PMI rose to 52.9 in March, the steepest pace in activity since June 2022, reflecting the dissipating impact of the pandemic.

Currencies

The Australian dollar (AUD) continued to descend over the month of March, closing -1.8% lower in trade weighted terms to 60.3. The AUD depreciated relative to all four major currencies referenced in this update.

The trading range of the AUD/USD tightened over March after being elevated for the first two months of the year. Volatility continued to be dominated by global central bank interest rate policy and inflation indicators, in addition to the emergence of a potential banking crisis with the collapse of Silicon Valley Bank (SVB).

Relative to the AUD, the Japanese Yen (JPY) led the pack in March, appreciating by 3.2%. Conversely, the US dollar (USD) was the laggard of the month, albeit with a positive relative return of 1.0% relative to the AUD. Year-on-year, the AUD is now weaker than the USD, Euro (EUR), Pound Sterling (GBP) and JPY by – 10.8%, -8.8%, -5.0% and -2.6%, respectively.