Monthly Market Review – December 2021

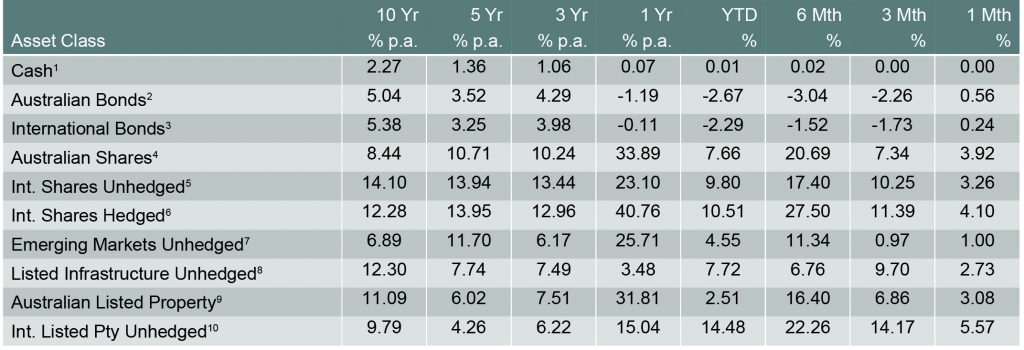

VIEW PDFHow the different asset classes have fared (As at 31 December 2021)

1 Bloomberg AusBond Bank 0+Y TR AUD, 2 Bloomberg AusBond Composite 0+Y TR AUD, 3 Bloomberg Barclays Global Aggregate TR Hdg AUD, 4 S&P/ASX All Ordinaries TR, 5 Vanguard International Shares Index, 6 Vanguard Intl Shares Index Hdg AUD TR, 7 Vanguard Emerging Markets Shares Index, 8 FTSE Developed Core Infrastructure 50/50 NR AUD, 9 S&P/ASX 300 AREIT TR, 10 FTSE EPRA/NAREIT Global REITs NR AUD Source: Centrepoint Research Team, Morningstar Direct

International Equities

Unhedged and hedged international equities exposures finished positive on the month of December, changing 3.98% and 1.73% respectively. Even with high inflation numbers and surging Omicron case numbers, international equities rose to finish the year. A gain in the AUD/USD caused by a rebound in the iron ore price, which is highly correlated to the AUD, meant slight divergence in the hedged and unhedged returns.

Australian Equities

The S&P/ASX All Ordinaries Index rose by 2.67% in December to finish the year strong. Fears regarding the Omicron variant subsided from the previous month as markets didn’t believe the economic impacts from the outbreak would cause economic damage like the previous variants. This had a lot to do with the governments “learn to live with it” reaction to the virus.

Domestic and International Fixed Income

Australian long and short-term bond yields remained mostly unchanged on the month as the index rose 0.09%. International bonds fell 0.44% on the month as the US 10-year bond rose slightly on the month, differing from the Australian market. The Federal Reserve is likely initiating rate hikes in March this year which slightly pushed up these yields.

Australian Dollar

The Australian Dollar rose 1.8% on the quarter as a bounce in the iron ore price provided support. The Aussie Dollar is still in a gradual downtrend over the one year as it fell ~6% across 2021. This was primarily driven by a significant fall in the iron ore price from the fall in demand in the commodity primarily from China. The correlation between this commodity and the AUD is significant as it is Australia’s most exported resource.

Disclaimer

The information provided in this communication has been issued by Centrepoint Alliance Ltd and Ventura Investment Management Limited (AFSL 253045).

The information provided is general advice only has not taken into account your financial circumstances, needs or objectives. This publication should be viewed as an additional resource, not as your sole source of information. Where you are considering the acquisition, or possible acquisition, of a particular financial product, you should obtain a Product Disclosure for the relevant product before you make any decision to invest. Past performance does not necessarily indicate a financial product’s future performance. It is imperative that you seek advice from a registered professional financial adviser before making any investment decisions.

Whilst all care has been taken in the preparation of this material, no warranty is given in respect of the information provided and accordingly neither Centrepoint Alliance Ltd nor its related entities, guarantee the data or content contained herein to be accurate, complete or timely nor will they have any liability for its use or distribution.