Treasurer Josh Frydenberg says rising confidence and a further unexpected drop in the unemployment rate are another sign there will be a strong economic recovery when virus lockdowns come to an end.

Treasurer Josh Frydenberg says rising confidence and a further unexpected drop in the unemployment rate are another sign there will be a strong economic recovery when virus lockdowns come to an end.

Spring has finally arrived and it’s the perfect time to refresh, reset and declutter your finances.

Income protection cover protects your most valuable asset – your ability to earn an income.

The Government is continuing to tighten the eligibility rules for claiming tax concessions relating to small business capital gains tax (CGT) obligations.

If you qualify, these concessions can have a big impact on how much of the profit from the sale of a business asset you get to keep, and how much goes to the taxman.

Given the generous nature of the concessions, the ATO is keen to ensure they are used appropriately.

Selling an income-producing asset such as property, business equipment or shares at a profit, will create an assessable capital gain. This capital gain is then used to calculate your CGT obligation, which forms part of your annual income tax bill.

Business owners are permitted to use several tax concessions to reduce their CGT obligation, but the eligibility rules can be tricky to navigate.

A new tax determination (TD 2021/2) has further tightened them by clarifying that companies carrying on a business whose only activity is renting out an investment property are not eligible to claim the CGT concessions when the property is sold.

Although this ruling is a big loss for some property investors, it’s worth remembering that if you do qualify, these concessions can substantially reduce – or even eliminate – the CGT payable on the sale of business assets.

The four small business CGT concessions are in addition to the normal 50 per cent general discount on CGT applying when you have owned an asset for more than 12 months.

Generally, the concessions apply to any asset your business owns and eventually sells at a profit, provided your annual turnover is under $2 million.

The four small business CGT concessions are:

If your business turnover is over $2 million but under $10 million, you may be able to use the small business restructure rollover concession. This permits the transfer of active assets – including CGT assets, trading stock and depreciating assets – from one business entity to another without incurring an income tax liability.

You can apply for as many of the four special CGT concessions as you are entitled to. In some situations, this can reduce your capital gain to zero. Before applying, you need to meet the basic eligibility conditions for the CGT concessions.

As the release of TD 2021/2 shows, the government regularly tightens the eligibility criteria for these concessions, so if you plan to take advantage of them, ensure you check the qualifying requirements carefully – or speak to us – as the process is quite complex.

Put simply, you must satisfy four basic conditions applying to all the concessions and then check if you meet the additional eligibility rules applying to each CGT concession.

The first condition requires you to be either a small business entity (SBE) with an aggregated turnover of less than $2 million; not carrying on a business but have a ‘passively-held asset’ used in the business as a connected entity; a partner in an SBE partnership; or satisfy the maximum net asset value ($6 million) test.

In addition, the business asset you are disposing of must satisfy the active asset test. If the asset is a share in a company or an interest in a trust, it must meet additional conditions.

The final step covers assets related to membership interests in a partnership. Each step must be considered in the set order before moving to the eligibility criteria for the individual concessions.

If you would like more information about the tax implications surrounding the disposal of your business assets, call us today.

The tough trading conditions resulting from COVID-19 mean Nasir has decided to downsize his trucking business. He sells an active asset, which is a haulage vehicle he has owned for four years. As a result, he makes a capital gain of $80,000.

At the same time, he makes a separate capital loss of $10,000 when he sells another smaller piece of equipment.

As Nasir satisfies all the eligibility conditions for the normal CGT discount and the small business 50% active asset reduction concession, his capital gain position for these assets is:

| Capital gain | $80,000 |

| Capital loss | $10,000 |

| Take the capital loss away from the capital gain | $70,000 |

| Apply 50% CGT discount ($70,000 x 50%) to the remaining capital gain | $35,000 |

| Apply 50% small business active asset reduction ($35,000 x 50%) to the remaining capital gain | $17,500 |

| Reduced capital gain | $17,500 |

Nasir may be able to further reduce his $17,500 (reduced) capital gain if he satisfies the conditions applying to both the small business retirement exemption and the rollover concession.

* This case study is for illustrative purposes only. Please seek advice for your specific circumstances.

Legislation has passed, taking effect from 1 July 2021, which increases the number of members allowed in an SMSF from 4 to 6. How could this impact you?

Inheritance is an emotional subject on every level. The people leaving an inheritance generally do it with pride and love. The people receiving an inheritance often receive it with gratitude – and sorrow. But while emotional, it’s also a financial transfer that comes with a whole range of legal, financial planning and admin issues attached.

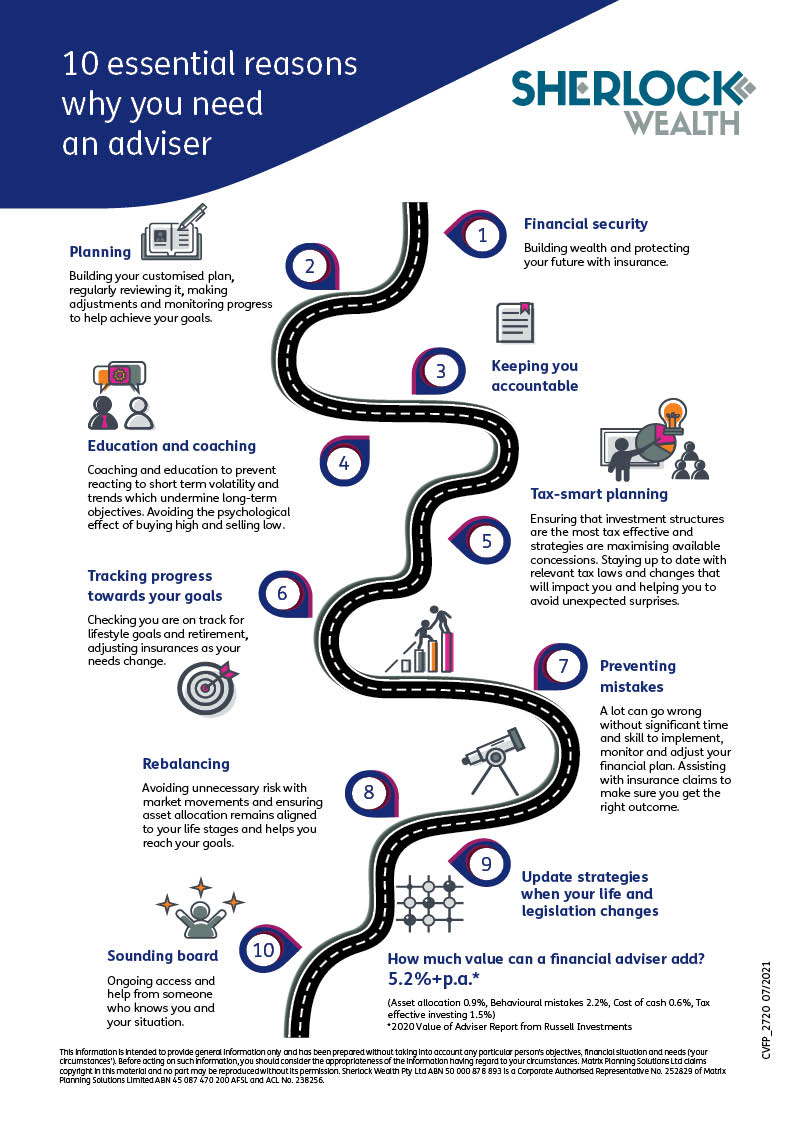

If you are not sure when to seek financial advice, here are 10 essential reasons why you need should get started.

If you were planning the trip of a lifetime, no doubt you’d make a list of all the things you wanted to see and do. We help people just like you with questions like these.

Financial protection for your loved ones when you die

Sudden death can place financial stress on those who depend on you. If this happens, life cover can help them pay the bills and other living expenses.

What is life cover?

Life cover is also called ‘term life insurance’ or ‘death cover’. It pays a lump sum amount of money when you die. The money goes to the people you nominate as beneficiaries on the policy. If you haven’t named a beneficiary, the super trustee or your estate decides where the money goes.

Life cover may also come with terminal illness cover. This pays a lump sum if you’re diagnosed with a terminal illness with a limited life expectancy.

Accidental death insurance is different from life cover. It will only payout if you die from an accident. It will not provide cover if you die from an illness, disease or suicide. This type of cover often has a lot of exclusions.

To understand what’s covered under a policy and the exclusions, read the Product Disclosure Statement (PDS).

Decide if you need life cover

If you have a partner or dependents, life insurance can help repay debt and cover living costs if you die.

If you don’t have a partner or people who depend on you financially, you may not need life cover. But consider getting trauma insurance, income protection insurance or total and permanent disability (TPD) insurance in case you get sick or injured.

How much life cover you might need?

To decide how much life cover to get, consider how much money you or your family would:

The difference between these is the amount of cover you should get.

Use our Life insurance calculator

Work out if you need life insurance and how much cover you might need.

If you need help deciding if you need life cover, reach out to the Sherlock Wealth team for assistance here.

How to buy life cover

Check if you already hold life insurance through super. Most super funds offer default life cover that’s cheaper than buying it directly. You can increase your level of cover through your super fund if you need to.

You can also buy life cover from:

Life cover can be bought on its own or packaged with trauma, TPD or income protection insurance. If it’s packaged, your life cover may be reduced by any amount paid on other claims in the package. Check the PDS or ask your insurer.

Before buying, renewing or switching insurance, check if the policy will cover you for claims associated with COVID-19.

Life cover premiums

You can generally choose to pay for life cover with either:

Your choice of stepped or level premiums has a large impact on how much your premiums will cost now and in the future.

Compare life cover.

Once you know how much life cover you need, shop around, and compare:

A cheaper policy may have more exclusions, or it may become more expensive in the future. You can find information about the policy on the insurer’s website or in the Product Disclosure Statement (PDS).

Use our Life insurance claims comparison tool

Compare how long it takes different insurers to pay a life cover claim and the percentage of claims they pay out.

What you need to tell your insurer

You need to tell your insurer anything that could affect their decision to insure you. You need to give them this information when you apply, renew or change your level of cover.

Insurers usually ask for information about your:

If an insurer doesn’t ask for your medical history, it may mean that the policy has more exclusions.

The information you provide will help the insurer to decide:

It is important that you answer the questions honestly. Providing misleading answers could lead an insurer to deny a claim you make.

Making a life cover claim

If someone close to you dies and you need to make a claim, or if you need to make a terminal illness claim, see how to make a life insurance claim.

If you would like help reviewing or selecting appropriate life insurance cover, please reach out to the Sherlock Wealth team here to help you look at what’s right for you.

Source: MoneySmart

(ASIC)

No one likes to think about the distress it will cause their loved ones or what kind of burden they’ll be left with. That’s why death is often considered a taboo topic of conversation, along with money and politics.